More about the book

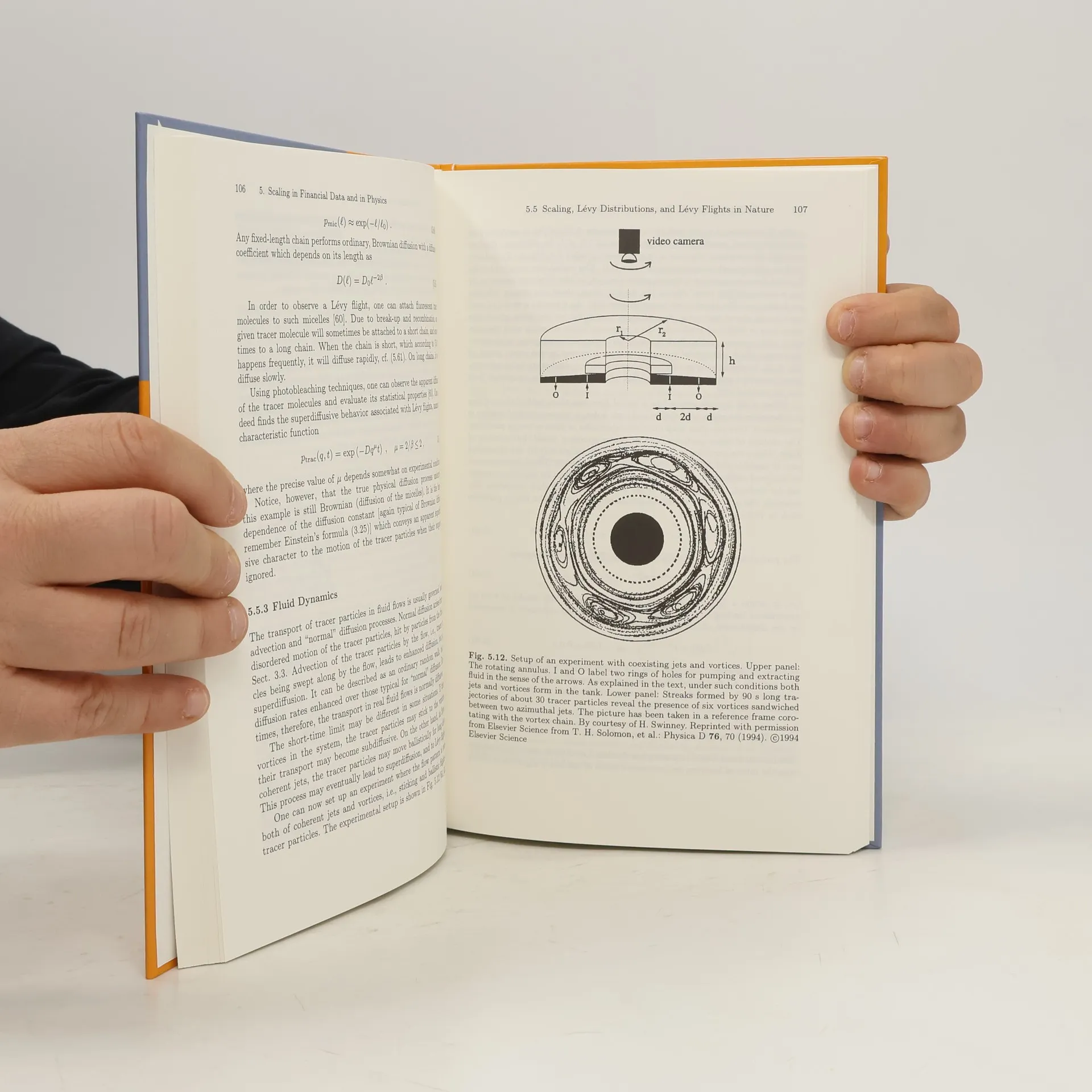

A careful examination of the interaction between physics and finance. It takes a look at the 100-year-long history of co-operation between the two fields and goes on to provide new research results on capital markets - taken from the field of statistical physics. The random walk model, well known in physics, is one good example of where the two disciplines meet. In the world of finance it is the basic model upon which the Black-Scholes theory of option pricing and hedging has been built. The underlying assumptions are discussed using empirical financial data and analogies to physical models such as fluid flows, turbulence, or superdiffusion. On this basis, new theories of derivative pricing and risk control can be formulated.

Book purchase

The statistical mechanics of capital markets, Johannes Voit

- Language

- Released

- 2001

- product-detail.submit-box.info.binding

- (Hardcover)

Payment methods

We’re missing your review here.

- Title

- The statistical mechanics of capital markets

- Language

- English

- Authors

- Johannes Voit

- Publisher

- Springer

- Released

- 2001

- Format

- Hardcover

- Pages

- 220

- ISBN10

- 3540414096

- ISBN13

- 9783540414094

- Series

- Tags

- Non-Fiction, Textbooks, Business, Business & Management, Natural sciences, Science, Economics, Math Textbooks, Finance, Physics Textbooks

- Rating

- 4.2 out of 5

- Description

- A careful examination of the interaction between physics and finance. It takes a look at the 100-year-long history of co-operation between the two fields and goes on to provide new research results on capital markets - taken from the field of statistical physics. The random walk model, well known in physics, is one good example of where the two disciplines meet. In the world of finance it is the basic model upon which the Black-Scholes theory of option pricing and hedging has been built. The underlying assumptions are discussed using empirical financial data and analogies to physical models such as fluid flows, turbulence, or superdiffusion. On this basis, new theories of derivative pricing and risk control can be formulated.