More about the book

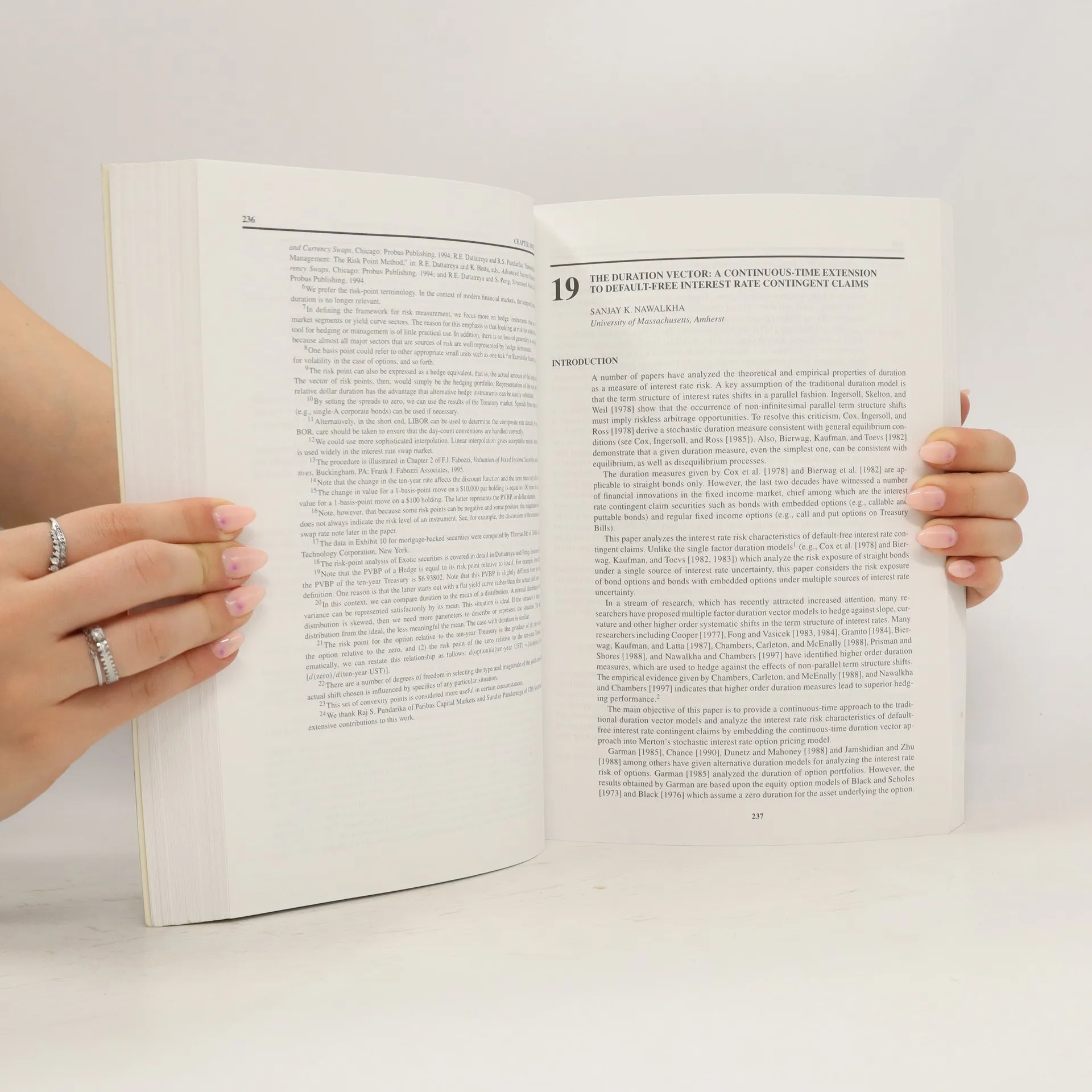

Institutional Investor Inc. introduces the most comprehensive volume of leading research on how to analyze, manage and measure interest rate risk. Interest Rate Risk Measurement and Management presents a unique collection of the key contributions in fixed-income investment research. This complete practitioners' manual showcases every major topic in interest rate risk management with detailed analyses and full treatment of equations and statistical measures. It is a substantial investment resource on: Single and Multi-factor Duration Risk Measures Interest Rate Risk Models for Fixed Income Derivatives Interest Rate Risk Models for Depositories, Thrifts, the FDIC, Insurers and Pension Funds As the most current and extensive collection of research written for professionals, Interest Rate Risk Measurement and Management belongs on the desk of every: Bond Portfolio Manager - Bond Analyst - Bond Strategist Derivatives Specialist - Risk Manager - Corporate Pension Fund Manager - Financial Institution Executive - and Bank Regulator.

Book purchase

Interest Rate Risk Measurement and Management, Donald R. Chambers, Sanjay K. Nawalkha

- Language

- Released

- 1999

- product-detail.submit-box.info.binding

- (Paperback)

Payment methods

No one has rated yet.

- Title

- Interest Rate Risk Measurement and Management

- Language

- English

- Authors

- Donald R. Chambers, Sanjay K. Nawalkha

- Publisher

- I.I. Books

- Released

- 1999

- Format

- Paperback

- Pages

- 568

- ISBN10

- 0961944692

- ISBN13

- 9780961944698

- Series

- Description

- Institutional Investor Inc. introduces the most comprehensive volume of leading research on how to analyze, manage and measure interest rate risk. Interest Rate Risk Measurement and Management presents a unique collection of the key contributions in fixed-income investment research. This complete practitioners' manual showcases every major topic in interest rate risk management with detailed analyses and full treatment of equations and statistical measures. It is a substantial investment resource on: Single and Multi-factor Duration Risk Measures Interest Rate Risk Models for Fixed Income Derivatives Interest Rate Risk Models for Depositories, Thrifts, the FDIC, Insurers and Pension Funds As the most current and extensive collection of research written for professionals, Interest Rate Risk Measurement and Management belongs on the desk of every: Bond Portfolio Manager - Bond Analyst - Bond Strategist Derivatives Specialist - Risk Manager - Corporate Pension Fund Manager - Financial Institution Executive - and Bank Regulator.